The global economy has been decimated by COVID-19. While governments continue to try and contain the pandemic, industries and societies have had to adapt. Futuresource’s third COVID-19 update reflects on progress governments have made towards addressing the economic impact; this includes how the Consumer Electronics, Entertainment and Pro-AV markets have fared in H2, as well as what the indications are for H1 2021.

The promising news coming from COVID-19 vaccine trials has provided industries and citizens with the hope that we might be about to turn the corner, but the impact and disruption to socio-economic trends will likely be with us for some time. In June, when Futuresource last wrote about the impact COVID-19 was having on technology sectors, the outlook was for market disruption to continue through the second half of 2020, with both demand and supply-side issues not being fully resolved until H1 of 2021. We were expecting as much as $120bn to be wiped off the retail value of Consumer Electronics, Entertainment and Pro-AV markets by the end of 2020.

Where there were uncertainties in H1 of 2020, governments have stepped in and provided support; it is estimated that globally, more than 50 million jobs have been retained due to direct government support. Thanks to the success of national lockdowns the spread of the virus had slowed enough that by the end of H1 2020, governments had rolled back restrictions on trade and mobility to encourage consumers and workers to return to pre-COVID-19 patterns. However, since then cases have risen once more, forcing governments to implement short term national lockdowns or localized approaches.

The second wave notwithstanding, the combination of government support and easing of lockdowns has softened the economic impact. In H1, forecasters were estimating that the pandemic would lead to a 7.6% decline in the global economy. Forecasts have since been revised and it is now thought that the global economy will shrink by 7.2%, a slight improvement. However, this level of support has come at a cost. Globally, government debt is now on average equivalent to 76% of GDP.

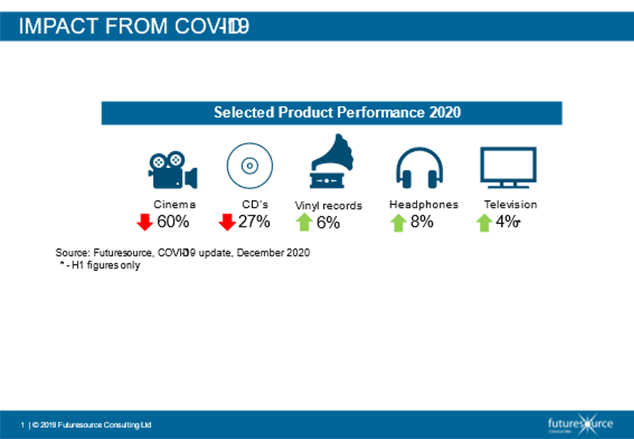

Have government actions been enough to revive those markets most impacted in H1 from the pandemic? Currently it appears not. Areas such as box-office and live events remain subdued. The reliance of pay-tv on key events, many of which have been cancelled or scaled back, has led to an overall decline in ARPU. Instead, consumers are subscribing to media content via on demand services and Futuresource forecast spend on premium video on demand (PVOD) will top $500 million by the end of 2020.

Media consumption is not the only area where we have seen significant changes in channel preferences by consumers. Industries that have previously been slow to adopt digital channels in comparison to consumer facing enterprises have had to catch up. At the same time, vendors with large retail outlet footprints have had to consider how to blend online experiences with existing channels, with stores modifying customer engagement strategies to include curb-side pick and digital signage.

2020 has not only left a lasting mark on consumers; it has also led to a shift in the relationship between work and technology. With two thirds of enterprises allowing employees to work from home, the home working genie is well and truly out of the bottle and it is difficult to see it going back. Vendors are starting to place big bets on the integration of collaboration and communication tools with enterprise systems, as evidenced by the recent announcement that Salesforce is looking to acquire Slack (a work-based chat and collaboration platform) for $27.7 billion. For the rest of the sector, 2020 was a year of two halves. In H1, demand far outstripped the ability of vendors to supply devices, while H2 saw a gradual return to more rational patterns of demand.

2020 might have been a particularly difficult year for vendors, and while at least from a global trade perspective we are likely to see a return to normality in H1 2021, the trends of 2020 are set to accelerate next year. Vendors of consumer technology and media will need to confront the lack of investment into online channels, as well as the low cost of sourcing goods and switching enabled by digital channels by developing customer experience programs. For enterprises, investment in digital tools is now a priority. Enterprises are having to use technology to be able to react faster to unpredictable changes by enabling teams to maintain productivity no matter where they are working from.