The evolution of premium streaming video on demand has seen different phases of development condensed into less than two years since the start of the pandemic. As indicated within our research at Futuresource Consulting, a total of 500 million subscription video on demand (SVoD) subscribers have been added since the end of 2019, highlighting how premium streaming behaviour has accelerated or been reinforced across all corners of the globe. New services have launched, driven by the continued drive of D2C services, along with international expansion. However, the anticipated slowdown in streaming video subscriber uptake was realised in 2021, with major players including Netflix and Disney+ both reporting a significant, but not unexpected slowdown, as consumers effectively brought their decision to take a service forward from 2021 to 2020.

Further underlying consumer behaviour also suggests a potential shift in how consumers manage their SVoD services and that the days of prolific ‘service stacking’, particularly in well established markets such as the USA, may be over.

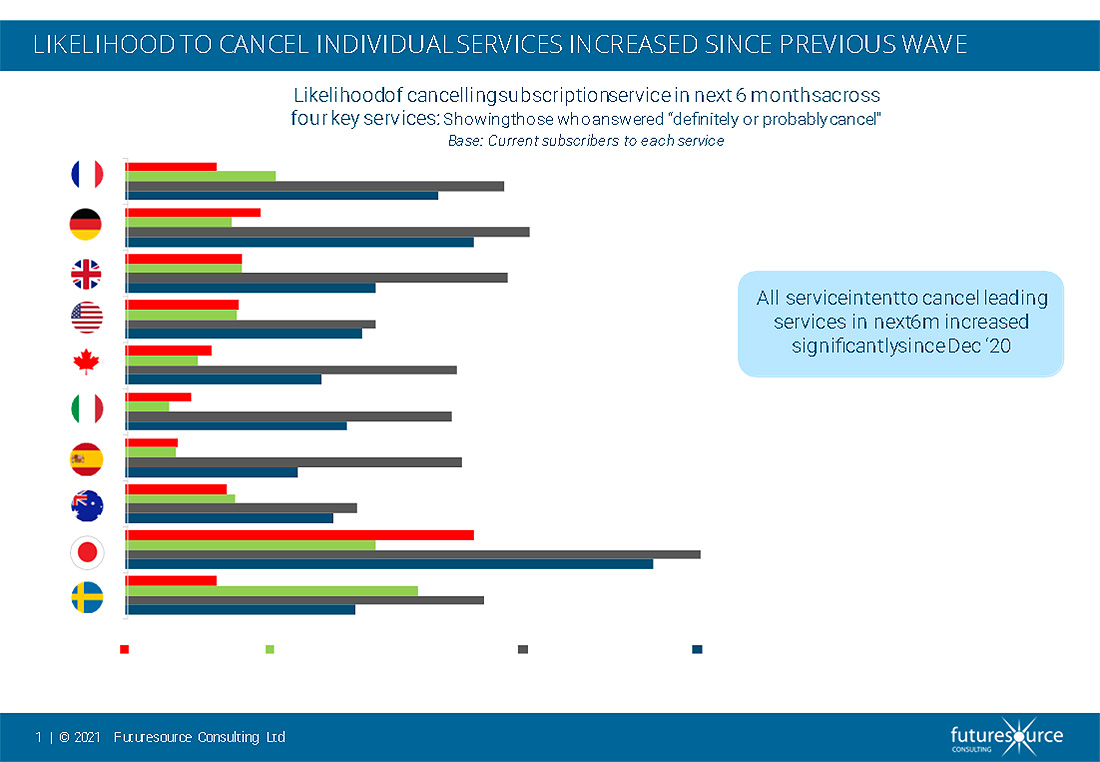

Futuresource’s Living With Digital consumer research from 2021 highlights that consumers are thinking differently about their SVoD portfolios, meaning that churn management from SVoD providers will remain as pertinent as subscribe acquisition for the foreseeable future. There was a notable increase in intent to cancel services in H2 2021 compared to the previous two surveys undertaken. This was evident across all types of services, with even the ‘utility’ platforms of Netflix and Amazon Prime Video seeing a marked increase in intent to cancel. Although carry through on this intent is likely to be much lower, with service bundling and general apathy towards the cancellation process helping reduce this actual cancellation rate, this shift in mentality is still quite striking. This is particularly significant when considering that typically over a quarter of SVoD subscribers said they will cancel and restart services more in the next year than they do now, effectively ‘dipping in and out more’.

Whilst the increased intent to cancel and switching of services provides a more negative outlook, this is contrasted by the fact that around one-third of European SVoD subscribers and over 40% of US SVoD subscribers say they will take at least one more SVoD service in the next 12 months than they do now – an increase since the last wave. This demonstrates that the thirst for new services and content has not dried up since the easing of restrictions. These combined findings potentially point towards a future of service surfing rather than service stacking, whereby subscribers will continue to add new services and may consider replacing an existing one, rather than adding it on top. Therefore the boom in multiple service uptake witnessed in 2020 will continue to slow, at least in terms of taking multiple services simultaneously.

It is also important to remember that SVoD service adoption and usage is not to be considered in isolation. In terms of consumers’ streaming video service portfolios, SVoD services sit alongside a new wave AVoD services such as Pluto TV, particularly in the USA, as well as broadcaster VoD (BVoD) services such as BBC iPlayer in Europe. Not forgetting transactional digital video services, Pay-TV/cable and traditional video viewing. We also know that the more SVoD services consumers take, the more likely they are to consume content on these other platforms.

The new wave of AVoD services and FAST channels have generated considerable headlines and are now part of many consumers regular viewing in the USA, with over 40% of US consumers watching an AVoD service at least monthly. While international expansion has also been evident from key services, uptake in Europe has proved more challenging. A strong BVoD legacy, more limited local content and a fragmented advertising and broadcast landscape across the region means that user growth will be increasingly reliant on partnerships with TV manufacturers and possibly across the longer term, local broadcasters.

With new streaming video services still rolling out, the landscape will continue to become increasingly fragmented in 2022, as will consumers’ video consumption. In order to provide a seamless viewing experiences, the topic of super aggregators across all different business models becomes as significant as it ever has been. With the largest media and tech companies all staking a claim to be the ultimate super aggregator, 2022 could well be as intriguing a year in the streaming video landscape as any we have seen of late.